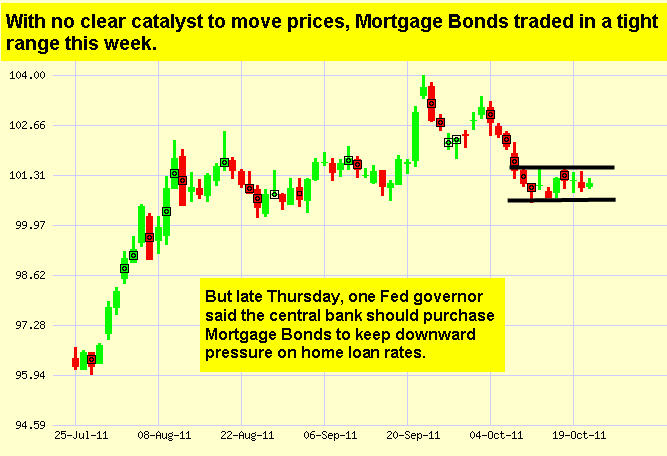

Don’t Say Another Word! 5 Secrets to Leaving More Effective Voice Messages People are busy. That means, even with the wide variety of technical products developed to keep us in touch, it’s sometimes hard to get a hold of people. In those instances, we find ourselves transported back to the tried-and-true technology of the 1980s—that is, leaving a message after the beep. Same Old, Same Old While the technology has changed from tapes to megabytes, the basic concept of a voice message remains the same. You talk; it records; people listen. Sadly, that’s not the only thing that’s the same. Many people still don’t know how to leave a message that provides information but also establishes a compelling reason for the listener to call back. Use These Tips Today! The following tips can help you be more effective and get better results with voice messages: 1. Don’t Talk So Much. You have a limited window to make your point. That means you can’t provide a lot of background information or cover multiple topics. Before you call, make sure you have a singular focus to mention if you get the person’s voicemail. Then, highlight that important point, and leave the rest of your points for the actual follow-up discussion. 2. Focus on a Problem. To put it bluntly: People don’t want to hear about you; they want to hear about themselves. So before you call, make sure you’ve thought about the person on the other end—including what she cares about, what she spends her time on, as well as what she wishes she could spend her time on instead. You could even try to imagine why she was busy and couldn’t answer the phone. Or imagine where she’s about to rush off to as soon as your message ends. Based on those ideas, craft a simple, focused message that hits on ONE major problem or issue that the listener has. 3. Everyone Likes a Good Mystery. Once you’ve focused on a single overriding problem, resist the temptation to go into your sales pitch about solving it. For one thing, the listener probably doesn’t have time (or want) to listen to your pitch. For another, if you give your pitch, what reason do they have to call you back? Instead, only allude to the idea that a solution does exist…but don’t go into detail. Leave some mystery. That’s your hook for getting them to actually call you back…because now they actually have a reason to! Finally, state a number the person can reach you at and say you’d like to tell/give them some information by chatting for a couple of minutes. You can even give them a time frame (such as saying they can call you back by a certain day or time) to help create a sense of urgency about solving the mystery you’ve established in your message. 4. Energy and Enthusiasm. Nobody wants to listen to a person who’s boring or sounds bored. The same is true with voice messages. After all, if you don’t have energy when talking about something, why should the listener have the energy to call you back? So before you call, take a second to raise your energy level. Some experts recommend standing up when making a call or smiling while talking on the phone, as a way to subtly convey a pleasant, energetic tone. 5. Phone Home. It’s not enough to practice in your head. It’s not even enough to practice out loud. You need to actually leave some practice messages. So here’s what you do: call your home phone and leave some test messages. You can even try a few different approaches. When you get home, take notes about what worked and what you want to improve. Then, try the same process the next day or even every couple of months to make sure you’re still effective. Remember: If you don’t want to listen to yourself or don’t feel compelled to call back, then why would anyone else? By following these tips and constantly working to improve your voice message skills, you can help increase your productivity and the number of responses you receive. Economic Calendar for the Week of October 24 - October 28

Date | ET | Economic Report | For | Estimate | Actual | Prior | Impact |

Tue. October 25 | 10:00 | Consumer Confidence | Oct | 46.0 |

| 45.4 | Moderate |

Wed. October 26 | 08:30 | Durable Goods Orders | Sept | -1.0% |

| -0.1% | Moderate |

Wed. October 26 | 10:00 | New Home Sales | Sept | 300K |

| 295K | Moderate |

Thu. October 27 | 08:30 | Pending Home Sales | Aug | -1.0% |

| -1.2% | Moderate |

Thu. October 27 | 08:30 | GDP Chain Deflator | Q3 | 2.5% |

| 2.5% | Moderate |

Thu. October 27 | 08:30 | Gross Domestic Product (GDP) | Q3 | 2.2% |

| 1.3% | Moderate |

Thu. October 27 | 08:30 | Jobless Claims (Initial) | 10/22 | 403K |

| 403K | Moderate |

Fri. October 28 | 08:30 | Personal Income | Sept | 0.3% |

| -0.1% | Moderate |

Fri. October 28 | 08:30 | Personal Spending | Sept | 0.6% |

| 0.2% | Moderate |

Fri. October 28 | 08:30 | Personal Consumption Expenditures and Core PCE | Sept | 0.1% |

| 0.1% | HIGH |

Fri. October 28 | 08:30 | Personal Consumption Expenditures and Core PCE | YOY | NA |

| 1.6% | HIGH |

Fri. October 28 | 08:30 | Employment Cost Index (ECI) | Q3 | 0.6% |

| 0.7% | HIGH |

Fri. October 28 | 10:00 | Consumer Sentiment Index (UoM) | Oct | 57.5 |

| 57.5 | Moderate |

|

|