| "Twist and shout." Operation Twist is back on the table after the Fed said last week that it is extending the program. But will this decision – or the Fed’s lowered forecasts for US growth and inflation – be cause for shouting? Read on for details.  The week began with The week began with speculation that the Fed would extend “Operation Twist” after its two-day meeting of the Federal Open Market Committee. Remember, Operation Twist is where the Fed sells its holdings of short-term securities and Notes and then purchases longer-term Notes and Bonds in order to try and lower longer-term rates even further. The Fed extended the program, which began last fall, because the Fed feels that access to cheaper money will help spur on economic growth. And while the Fed did not mention anything about another round of Bond buying (called Quantitative Easing, or QE3), they laid some groundwork for additional stimulus if necessary.

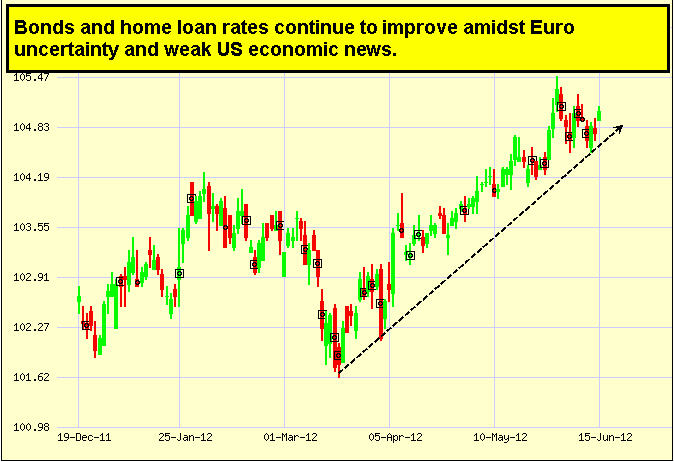

The Fed’s decision to extend Operation Twist – and their lowered forecasts for our economic growth – partly came from disappointing economic reports we’ve seen recently. The Fed noted that "growth in employment has slowed in recent months, and the unemployment rate remains elevated." Last week’s higher than expected Initial Jobless Claims exemplified that. In addition, the housing market continues to muddle along the bottom with numbers showing only modest improvement. Though there was some good news last week – even though Housing Starts were a bit below expectations, Building Permits (a sign of future construction) surged 8%. So what does all of this mean for home loan rates? Home loan rates continue to benefit from the drama in Europe and the weak economic reports here at home, as investors continue to see our Bonds (including Mortgage Bonds, to which home loan rates are tied) as a safe haven for their money. But it’s important to note that additional hints of QE3 could push Stock prices higher, shifting cash out of the Bond trade and hurting home loan rates in the process.

The bottom line is that now continues to be a great time to purchase or refinance a home, as home loan rates remain near historic lows. Let me know if I can answer any questions at all for you or your clients. |