How to Avoid Unnecessary Rental Car Fees You could end up doubling the daily rate unless you just say no at the counter. Renting a car is a little like buying a car: Before you can drive the vehicle off the lot, you have to withstand a hard sell for a slew of options. And in their zeal to nick your wallet, rental companies are getting creative. For example, you'll almost certainly get the pitch for prepaid gas. Presented as a convenience, it's a big moneymaker because you are likely to pay for fuel you never use. Thrifty, for one, makes it a tough option to turn down. When you fill up the car yourself, the company requires that you provide a receipt proving that the gas station was within ten miles of the rental car lot. If not, Thrifty hits you with a fueling charge.

If you prepay for a rental from Avis and change your mind, make sure you cancel at least 24 hours in advance; if you don't, you'll get your money back - minus a $50 "no show" fee. A few rental car companies even charge a fee of $15 if you return your car a day early.

Be aware of charges for add-ons, too. A portable GPS unit typically costs $13 a day, and satellite radio can trigger a $5 daily fee. An "electronic toll transponder" carries a daily or weekly fee - $3 a day is typical - in addition to the tolls. Need a car seat for your kid? That's another $11 a day.

If you're charged a fee that wasn't disclosed when you signed for the car or made an online reservation, fight it. Jeremy Acevedo, a research analyst at Edmunds.com and former Enterprise employee, says the squeaky wheel often gets the grease. Always pay with a credit card so you can dispute a charge if necessary. (If you use a debit card, a hold of $100 or more, plus the cost of the rental car, is often put on your account until the car is returned.)

The CDW decision. Nothing is as expensive, or as confusing, as the CDW, or collision damage waiver (sometimes called the LDW, or loss damage waiver). Agents are trained to make this rental car insurance, which typically costs $20 to $30 a day, sound nonnegotiable.

You probably don't need it. Rental car damage and liability are covered by your auto insurance policy up to the same limits as for your personal vehicle, and your credit card likely fills any gaps. Most cards, for example, will pick up your deductible and miscellaneous fees.

But turning down the CDW isn't a slam-dunk. Some people buy it because they don't want an accident on their insurance record, should one occur. And if you don't have auto insurance because you don't own a car, you may need to suck it up. Your credit card is likely to cover collision damage to the rental car, but no credit card covers you for liability - personal injury or property damage you cause and for which you are liable. Although liability insurance up to state limits is usually included automatically in the rental cost, the protection is often minimal. To beef it up, you'll have to buy a separate add-on called supplemental liability or additional liability insurance (for about $13 a day).

If you are in an accident and haven't purchased the CDW, the rental company may charge you towing, administrative and "loss of use" fees - the money the rental company forfeits by having a car in the shop instead of out on the road. And those fees aren't always covered by your insurance or credit card. Only a handful of states require that standard auto policies cover loss of use, and most major insurers don't cover it. Progressive does include it on standard policies, however, and State Farm sells an annual endorsement for $50 to $100.

Among credit cards, American Express and Visa cover towing, administrative and loss-of-use fees. But only certain MasterCards (gold, platinum, World and World Elite cards) cover rental cars; that coverage includes towing and loss of use, but not administrative fees. Discover doesn't cover any rental car fees.

Although you may be covered on paper for loss-of-use fees, you could get caught in the crossfire. Card issuers and insurers typically ask rental companies to prove loss of use by providing fleet logs showing that all other vehicles were rented out, but rental companies are often reluctant to turn over their records. It can come down to a gamble. Take the CDW, or take a chance that the stars won't align against you. Even if you are in an accident and no one else pays up for loss of use, you're likely to be charged a few hundred dollars at most. Shop smart. To save money on your rental, shop around. Your best bet is to make a reservation as soon as you know you're going to need a vehicle and then keep checking for lower prices as your departure approaches. Acevedo says walk-ups at the airport can get a steal if unreserved vehicles are sitting on the lot. If you won't owe a cancellation fee, ask for the best rate at several rental counters.

You can often save money at smaller companies, such as Ace Rent A Car and Midway, which may not show up on the big travel Web sites. Ace just scored J.D. Power's highest rating for overall satisfaction. (Enterprise scored the highest among the major brands; Avis and Thrifty scored the lowest.) If your goal is a low price and you're not picky about which company you rent from, try Priceline or Hotwire - they'll get you a reservation with a name brand for up to 40% off, but you won't find out which one until you're booked. Plus, you will have to prepay to get the lowest rates.

For longer trips, consider renting at an off-airport location. The airport concession fee is typically 11% to 13% of your total rate. Do the math to see whether a cab ride into town is worth the cost.

Reprinted with permission. All Contents ©2012 The Kiplinger Washington Editors. Kiplinger.com.

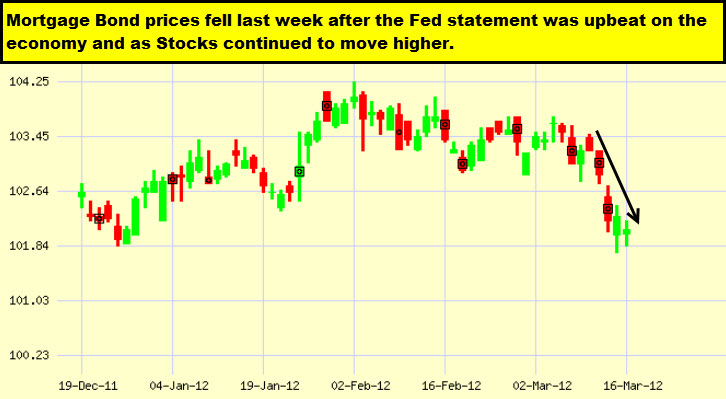

Economic Calendar for the Week of March 19 - March 23

Date | ET | Economic Report | For | Estimate | Actual | Prior | Impact |

Tue. March 20 | 08:30 | Housing Starts | Feb | NA |

| 699K | Moderate |

Tue. March 20 | 08:30 | Building Permits | Feb | NA |

| 676K | Moderate |

Wed. March 21 | 10:00 | Existing Home Sales | Feb | NA |

| 4.57M | Moderate |

Thu. March 22 | 08:30 | Jobless Claims (Initial) | 3/17 | 355K |

| 351K | Moderate |

Fri. March 23 | 10:00 | New Home Sales | Feb | 321K |

| 321K | Moderate |

|

|

interesting! although I have no expert, but I want have to know more and more, on your blog just interesting and useful information. Keep it up!

ReplyDelete