| They say that every cloud has a silver lining. And despite a slew of disappointing economic news last week, home loan rates continue to reach record best levels. Read on for details.  The majority of economic The majority of economic reports released last week added to the uncertainty about our economic outlook. Retail Sales fell more than expected while the NY State Manufacturing Index remains at relatively low levels. In addition, the National Association for Business Economics (NABE) reported that the outlook for job growth has fallen due to a weakening economy. The survey revealed that 23% on those polled in July think that US employment will rise over the next six months, down from 39% in April.

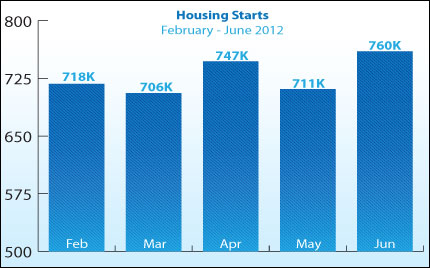

But the economic news wasn’t all negative. Inflation at the consumer level remained tame in July, while Housing Starts for June increased nearly 7% to 760,000. This marks the highest level for housing starts since October 2008. Since home builders don't start a house unless they are fairly confident it will sell upon its completion, if not before, changes in the rate of housing starts can tell us a lot about demand for homes and the construction outlook.

In other important news last week, Fed Chairmen Ben Bernanke was on Capitol Hill delivering his semi-annual testimony before both the Senate and House. He confirmed that our economy is weak, uncertainty in Europe is threatening U.S. growth, and unemployment is stubbornly high. But perhaps more significant was what Bernanke didn’t say: There was no mention or hint of another round of Bond buying (known as Quantitative Easing or QE3) at the next Fed Meeting.

It’s important to remember that rumors or hints of QE3 could help Bonds (and thus home loan rates, which are tied to Mortgage Bonds), but once an official announcement is made, Bonds and home loan rates could suffer as Stocks would likely rally. However, the weak economic data here and the continued problems in Europe mean that investors will likely continue to see our Bonds as a safe haven for their money…helping home loan rates in the process.

The bottom line is that home loan rates continue to reach historic lows, making now a great time to purchase or refinance a home. Let me know if I can answer any questions at all for you or your clients. |