A Simple Story:

How to Explain the Impact of Inflation on Home Loan Rates

In the wake of the Fed’s QE3 (or Quantitative Easing) announcement,

consumers may be wondering how this new effort to stimulate the economy

may impact the

mortgage and housing markets.

And they’d be right to wonder.

That’s because one of the consequences of QE3 could be inflation—which is the archenemy of Bonds and home loan rates.

Here’s a narrative you can use to explain to your clients why this is important…

Imagine for a moment that you are going to lend your very own money

to someone to buy a house. So you go through all the paces to determine

this person is

a good credit risk, you do the loan, and you start receiving $1,500

per month as your regular payment. You then of course take that $1,500

and start

loading up your shopping cart with the goods and services you need

on a monthly basis...food, clothing, medicine, gas, and so on.

But over time, you notice something happening…

Every month, you are getting slightly less in your cart than you did

the month before, for that same $1,500 you are spending. Why? Because

costs are on the

rise–that's inflation.

Now imagine that you are once again going to lend your very own

money to another person to buy a house. You go through all the paces

once again, and

determine that the person is a good credit risk.

You want the same shopping cart full of "stuff" that you got last

time in return for doing the loan, but this time you realize that you

can no longer get

that same cart full with $1,500. Due to inflation, you now need

$1,700 to buy those same goods and services.

As a result, you will need to charge a higher interest rate to

compensate you for the ongoing impact of inflation. This is why home

loan rates change when

there is a fear of inflation in the air.

Economic Calendar for the Week of October 08 - October 12

Date

|

ET

|

Economic Report

|

For

|

Estimate

|

Actual

|

Prior

|

Impact

|

| Wed. October 10 |

02:00

|

Beige Book |

Sept

|

|

|

|

Moderate

|

| Thu. October 11 |

08:30

|

Jobless Claims (Initial) |

10/6

|

NA

|

|

NA

|

Moderate

|

| Fri. October 12 |

08:30

|

Producer Price Index (PPI) |

Sept

|

NA

|

|

1.7%

|

Moderate

|

| Fri. October 12 |

08:30

|

Core Producer Price Index (PPI) |

Sept

|

NA

|

|

0.2%

|

Moderate

|

| Fri. October 12 |

10:00

|

Consumer Sentiment Index (UoM) |

Oct

|

NA

|

|

78.3

|

Moderate

|

|

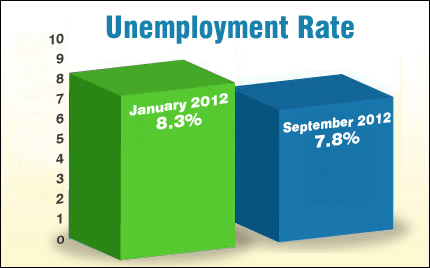

The Labor Department’s Jobs Report showed that 114,000 new jobs were

created in September, with 104,000 private sector job gains and 10,000

government job

gains. While this number was lower than expectations, the job

numbers for July and August were revised much higher.

The Labor Department’s Jobs Report showed that 114,000 new jobs were

created in September, with 104,000 private sector job gains and 10,000

government job

gains. While this number was lower than expectations, the job

numbers for July and August were revised much higher.