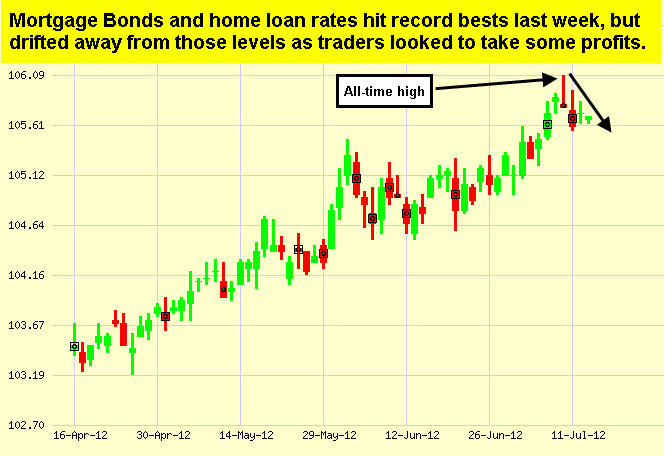

| Slow and steady wins the race. That may be true for certain Olympic events, but when it comes to our economy slowing seems to be the operative word of late. Read on for details and what they mean for home loan rates.

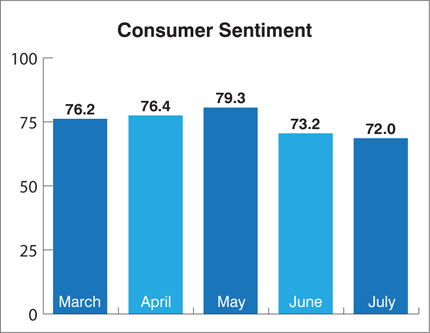

Last week there was more Last week there was more evidence of a slowing U.S. economy, as the National Federation of Independent Businesses stated that its small business optimism index saw its largest one-month drop in two years, falling 3 points to 91.4. The 91.4 number is the lowest level since October. Consumer Sentiment for July also came in at its lowest level this year.

Recession talk has grown in recent days, and some very well respected economists and thinkers believe we are either in a recession already or about to enter one. It is very tough to argue with this notion as the labor market and manufacturing numbers have rolled over in recent months, with those trends likely to continue lower in the face of so much uncertainty here and abroad. In addition, corporate earnings are starting to come out and companies are reporting numbers below already lowered guidance and citing uncertainty into the future.

So what does all of this mean for home loan rates? Recessions are deflationary (i.e. consumer prices moving lower) and deflation is good for Bonds as the fixed interest payment to the end investor goes further if consumer prices are moving lower. This means deflation is also good for home loan rates, as rates are tied to Mortgage Bonds.

If the economic data continues to be weak, the Fed will likely do another round of Bond buying, known as Quantitative Easing or QE3 – and in fact, the Fed Minutes for the June Meeting showed that a couple members had an appetite for more easing, but there was no consensus. Remember that additional hints of QE3 could initially push Stock prices higher, shifting cash out of the Bond trade and hurting home loan rates in the process. I will continue to monitor this situation closely.

The bottom line is that now continues to be a great time to purchase or refinance a home, as home loan rates continue to reach historic lows. Let me know if I can answer any questions at all for you or your clients. |

No comments:

Post a Comment