|

|

|

Last Week in Review: More

Fed chatter hit the wires about Quantitative Easing. Find out what

happened.

Forecast for the Week: The last week of February brings a full slate

of economic news.

View: Want your social media posts to be as effective as possible?

Don't miss important information below.

|

|

|

|

"You

don't know what you got until it's gone." Those

lyrics from the band Chicago's 1980's hit could apply to the chatter from

the Fed last week, as the debate about whether to continue their latest

round of Bond buying, known as Quantitative Easing, continues.

What

is Quantitative Easing? Quantitative Easing is the

concept of the Fed becoming a buyer of Treasuries and Bonds to try and

stimulate the economy. What

is Quantitative Easing? Quantitative Easing is the

concept of the Fed becoming a buyer of Treasuries and Bonds to try and

stimulate the economy.

Why does the Fed do Quantitative Easing? Oftentimes, the Fed

does Quantitative Easing when they are hoping to (1) create inflation and

avoid a deflationary economy, (2) lower the unemployment rate, and (3)

boost Stock prices. For this latest round of Quantitative Easing, the Fed

especially wanted to help stimulate the housing market and our economy

overall.

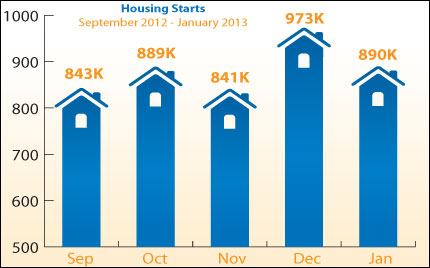

And the housing market has shown signs of improvement lately. While Housing

Starts in January declined overall, single family Housing Starts rose to

its highest rate since July 2008. Building Permits, a sign of future

construction, also came in above expectations. These reports were the latest

in a series of reports showing that the housing market is recovering.

What is all the Fed chatter about? Last week, the minutes

from the Fed's January meeting of the Federal Open Market Committee were

released. The minutes noted that several Fed members would like to halt the

Quantitative Easing program sooner than planned, because they are concerned

about inflation. However, it's important to note that last week's Producer

and Consumer Price Index Reports showed that inflation at both the

wholesale and consumer levels remained tame in January.

On the flip side, other Fed members are concerned that halting the program

too soon could end the recovery in the housing market, and hinder our

economic recovery overall. And given that the increase in the payroll tax

in January left consumers with less money in their paychecks, and that

Walmart has reported that February sales were the weakest in seven years,

this is an important factor to consider as well.

The biggest take away is that now remains a great time to consider a

home purchase or refinance, as home loan rates remain near historic lows.

Let me know if I can answer any questions at all for you or your clients.

|

|

|

|

|

Chart: Fannie Mae 3.0% Mortgage Bond (Friday Feb 22, 2013)

A

busy week of reports is ahead, with news on housing, manufacturing,

consumer sentiment, U.S. growth and inflation. A

busy week of reports is ahead, with news on housing, manufacturing,

consumer sentiment, U.S. growth and inflation.

- The week starts and ends with a measure of how the

consumer is feeling with Tuesday's Consumer Confidence Report

and Friday's Consumer Sentiment Index.

- There's a double dose of housing news on Tuesday,

with the Case Shiller Index and New Home Sales. Plus,

look for Pending Home Sales on Wednesday.

- We'll get a sense of how the economy is doing with

Wednesday's Durable Goods Orders, which measures orders for

products used for an extended period of time, and Thursday's Gross

Domestic Product, the biggest picture of economic activity.

- Also on Thursday, Weekly Initial Jobless Claims

will be reported.

- Ending the week, Friday brings Personal

Consumption Expenditures, the Fed's favorite measure of inflation,

along with Personal Income and Spending and the ISM Index.

Remember: Weak

economic news normally causes money to flow out of Stocks and into Bonds,

helping Bonds and home loan rates improve, while strong economic news

normally has the opposite result. The chart below shows Mortgage Backed

Securities (MBS), which are the type of Bond that home loan rates are based

on.

When you see these Bond prices moving higher, it means home loan

rates are improving -- and when they are moving lower, home loan rates are

getting worse.

To go one step further -- a red "candle" means that MBS worsened

during the day, while a green "candle" means MBS improved during

the day. Depending on how dramatic the changes were on any given day, this

can cause rate changes throughout the day, as well as on the rate sheets we

start with each morning.

As you can see in the chart below, Bonds and home loan rates remain steady

near record best levels. I'll continue to monitor them closely.

|

|

|

|

The Mortgage

Market Guide View...

|

|

|

|

|

Best

Days and Times for Posting to Social Media

More than nine out of ten businesses spend six or more hours online each

week maintaining a presence on social media. And while you probably already

know the benefits of social media--better engagement with your market,

better website traffic, improved sales--you might not realize that some

days (and times!) are better than others for posting to social media.

Social media analytics firm Socialbakers showed Facebook posts achieve 50% of their

total reach within 30 minutes of being posted. In other words, half of all

the people who will see your post have seen it within the first half-hour

after you post it. Not only that, by the time 90 minutes have elapsed, your

average post reaches less than 2% of total audience for the next seven

hours before it drops off completely.

That's why timing your posts properly is the best strategy. Here are the

best days and times to post according to current research from Social Caffeine:

Twitter

BEST: 1 p.m. to 3 p.m., Monday through Thursday

WORST: 8 p.m. to 9 a.m. Avoid after 3 p.m. Friday and weekends

Facebook

BEST: 1 p.m. to 4 p.m., peaking on Wednesdays at 3 p.m.

WORST: 8 p.m. to 8 a.m., avoiding weekends

LinkedIn

BEST: 7 a.m. to 9 a.m. OR 5 p.m. to 6 p.m., Tuesday through Thursday

WORST: 10 p.m. to 6 a.m., avoid Monday and Friday

Pinterest

BEST: 2 p.m. to 4 p.m. or 8 p.m. to 1 a.m., peaking on Saturday morning

WORST: 5 p.m. to 7 p.m. and late afternoons

Economic

Calendar for the Week of February 25 - March 01

|

Date

|

ET

|

Economic Report

|

For

|

Estimate

|

Actual

|

Prior

|

Impact

|

|

Tue. February 26

|

09:00

|

S&P/Case-Shiller

Home Price Index

|

Dec

|

6.5%

|

|

5.5%

|

Moderate

|

|

Tue. February 26

|

10:00

|

New Home Sales

|

Jan

|

385K

|

|

369K

|

Moderate

|

|

Tue. February 26

|

10:00

|

Consumer

Confidence

|

Feb

|

62.0

|

|

58.6

|

Moderate

|

|

Wed. February 27

|

08:30

|

Durable Goods

Orders

|

Jan

|

-4.0%

|

|

4.3%

|

Moderate

|

|

Wed. February 27

|

10:00

|

Pending Home

Sales

|

Jan

|

1.0%

|

|

-4.3%

|

Moderate

|

|

Thu. February 28

|

09:45

|

Chicago PMI

|

Feb

|

54.0

|

|

55.6

|

HIGH

|

|

Thu. February 28

|

08:30

|

Gross Domestic

Product (GDP)

|

Q4

|

0.5%

|

|

-0.1%

|

Moderate

|

|

Thu. February 28

|

08:30

|

Jobless Claims

(Initial)

|

2/23

|

360K

|

|

362K

|

Moderate

|

|

Fri. March 01

|

08:30

|

Personal Income

|

Jan

|

-2.3%

|

|

2.6%

|

Moderate

|

|

Fri. March 01

|

08:30

|

Personal

Spending

|

Jan

|

0.2%

|

|

0.2%

|

Moderate

|

|

Fri. March 01

|

08:30

|

Personal

Consumption Expenditures and Core PCE

|

Jan

|

0.2%

|

|

0.0%

|

HIGH

|

|

Fri. March 01

|

08:30

|

Personal

Consumption Expenditures and Core PCE

|

YOY

|

NA

|

|

1.4%

|

HIGH

|

|

Fri. March 01

|

10:00

|

ISM Index

|

Feb

|

52.4

|

|

53.1

|

HIGH

|

|

Fri. March 01

|

10:00

|

Consumer

Sentiment Index (UoM)

|

Feb

|

76.3

|

|

76.3

|

Moderate

|

|

|

|

|

The material

contained in this newsletter is provided by a third party to real estate,

financial services and other professionals only for their use and the use

of their clients. The material provided is for informational and

educational purposes only and should not be construed as investment and/or

mortgage advice. Although the material is deemed to be accurate and

reliable, we do not make any representations as to its accuracy or

completeness and as a result, there is no guarantee it is without errors.

As your mortgage

professional, I am sending you the MMG WEEKLY because I am committed

to keeping you updated on the economic events that impact interest rates

and how they may affect you.

is the copyright

owner or licensee of the content and/or information in this email, unless

otherwise indicated. does not grant to you a license to any content,

features or materials in this email. You may not distribute,

download, or save a copy of any of the content or screens except as

otherwise provided in our Terms and Conditions of Membership, for any purpose.

|

|

No comments:

Post a Comment